The global fashion wig market is being revolutionized, primarily fueled by the Generation Z (Gen Z) consumer, those born between 1996 and 2010. But for Gen Z, wigs aren't just beauty instruments and medical equipment, they're instruments of self-expression, exploration and social signaling. Gen Z accounted for 52% of global fashion wig sales in 2024, accelerating annual growth of 18%, versus 4.7% growth for the overall beauty industry (GMI, 2024).

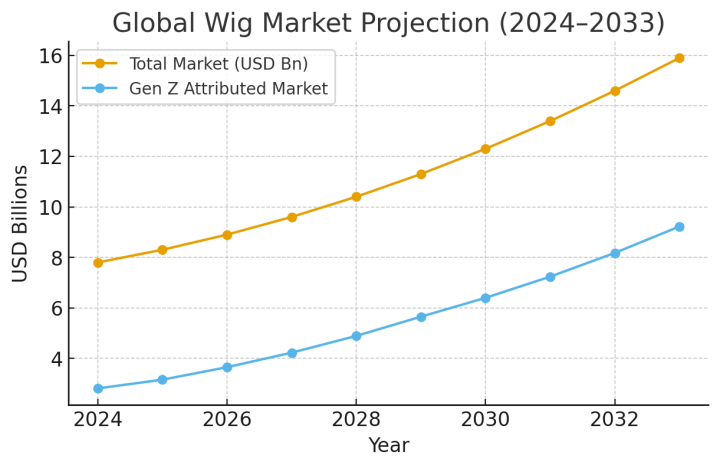

According to IMARC, Arizton, Mordor Intelligence, and ResearchAndMarkets, the global wigs and hair extensions market reached USD 7.5–8.1 billion in 2024 and is projected to grow to USD 14–15 billion by 2033. Gen Z contributes over half of incremental demand.

Three broad trends characterize the current and prospective market:

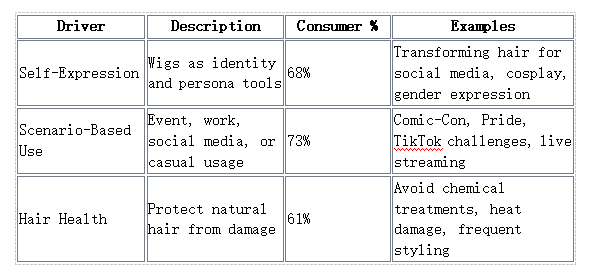

1. Self-Expression is Priority: Nearly 68% of Gen Z purchases are driven by identity building, such as experimenting with gender identity, cultural hairstyles and digital characters (McKinsey, 2019).

2. Consumption in Scenarios: Wigs are now indispensable in cosplay, K-pop fandom, social media content creation, live streaming, digital events and hybrid work, and that's driving a consumption pattern closely related to social situations(First Insight, 2023).

3. Sustainability Awareness: 42% of Gen Z view using biodegradable or recycled materials as the most important thing, and European and East Asian consumers are the most eco-aware. Sustainability is increasingly a key purchasing differentiator for consumers, and R&D and marketing strategies are being tailored accordingly.

Market Opportunities:

l Subcultural segments: LGBTQ+, cosplay, digital fandoms, fantasy fashion.

l Technological infusion: AR/VR virtual try-ons, AI-driven style recommendations, smart fibers.

l Hyper-localized production: On-demand production, culturally sensitive designs, regional distribution centers.

Strategic Imperatives: To capture Gen Z demand, brands need to bring the culture intelligence, supply chain agility, true community engagement, and product innovation, rather than simply trying to push them through the traditional mass-market approach.

Chapter 1: Gen Z Consumer Profiles and Behavioral Insights

1.1 Demographics and Digital Fluency

Population and Social Influence

The global Gen Z is about 2.5 billion and accounts for nearly 32% of the world's population. This generation was raised in a hyper-connected, digital-first world, and their social behaviors are so fluid and networked.

Key social media statistics:

Digital touchpoints: Before purchasing a wig, Gen Z usually interacts with 7–8 touchpoints, such as social media, influencer reviews, e-commerce sites, virtual try-ons, and friend suggestions (NielsenIQ, 2024).

1.2 Identity, Inclusivity, and Cultural Awareness

Identity is Fluid:

Wigs are seen as "liquid identity tools" that provide spaces for people to experiment with gender presentation, hair color and textures, and fashion in both physical and digital spaces.

The typical Gen Z wig enthusiast has 3-4 different wig styles to suit different needs (everyday style, social media creating, cosplay, events).

Inclusivity & Diversity:

l LGBTQ+ Gen Z buys wigs at 2.3x the rate of their heterosexual peers, and tend to gravitate toward styles that support gender expression (Cognitive Market Research, 2024).

l Multi-racial Gen Z shows strong fascination with hairstyles from African, East Asian, Latin American and Indigenous cultures.

Cultural respect:

l 57% of consumers research cultural origins before adopting traditional hairstyles.

l Brands that provide educational content on hairstyle history and cultural significance achieve 3.2x higher brand loyalty.

Price Sensitivity and Value Perception:

l While Gen Z rejects overt luxury pricing, $20–100 per unit is considered acceptable for quality and culturally respectful designs.

l Subscription models and limited editions are increasingly appealing due to perceived exclusivity and customization.

1.3 Core Motivations and Purchase Drivers

Scenario segmentation:

- Cultural events and fandom conventions: 32% of wig sales.

- Social media content creation: 28%, especially short-form video platforms.

- Daily style rotation and personal expression: 25%.

- Professional or performance-based settings: 15%.

1.4 Psychological Drivers

Social signaling:

Wigs serve as visual statements that express artistic, trend and subculture-related components.

Exploratory behavior:

Gen Z loves to experiment with aesthetics and can be seen trying up vibrant colors, textures and cultural styles.

Community validation:

l Approval from the peer community and influencer endorsement come as the top decision factor.

l Partnerships with micro-influencers result in 3.2x the engagement of traditional celebrity endorsements (Utry.dk, 2024).

1.5 Purchase Channels and Digital Interaction

Primary online channels:

Technology adoption:

l AR try-on: Increases purchase conversion by 28%.

l AI personalization: Style suggestions based on facial features, skin tone, and social media trends.

l Mobile-first UX: Simplified checkout, inventory visibility, and push notifications.

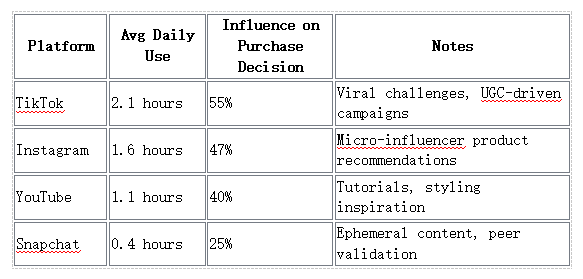

1.6 Social Media Influence and Community Dynamics

l TikTok: Hashtag challenges (#WigTransformation, #HairSwitch) amassed over 12B views worldwide and led to trend adoptions.

l Instagram: Micro-influencers have 3.2x higher engagement than media endorsements.

l YouTube: In-depth conversations on styling and caring for your wig raise confidence to buy by 47%.

l Discord/WhatsApp communities: Exclusive spaces for peer-to-peer sharing, limited edition drops, and event planning.

1.7 Future Behavioral Considerations

l Male and non-binary adoption: Increasing at a rate of 22% annually, due to the influence of gender-neutral aesthetics and involvement in cosplay.

l Virtual identity fusion: Gen Z are taking their exploration with avatars and virtual hair simulations, in the metaverse, and gaming platforms.

l Awareness of sustainability: The preference for recycled and biodegradable materials will increase over 50% by 2030 (GMI, 2024).

1.8 Summary of Gen Z Consumer Profile

l Digital-first, socially aware, culturally sensitive.

l Scenario-driven purchasing with a high degree of experimentation.

l Value-conscious but willing to pay for quality, authenticity, and sustainability.

l Highly influenced by peer validation, micro-influencers, and digital communities.

l Embraces technological innovation (AR/VR/AI) for a personalized shopping experience.

Chapter 2: Regional Market Analysis & Consumption Patterns

2.1 North America: Subculture Leadership and Innovation

Market Overview

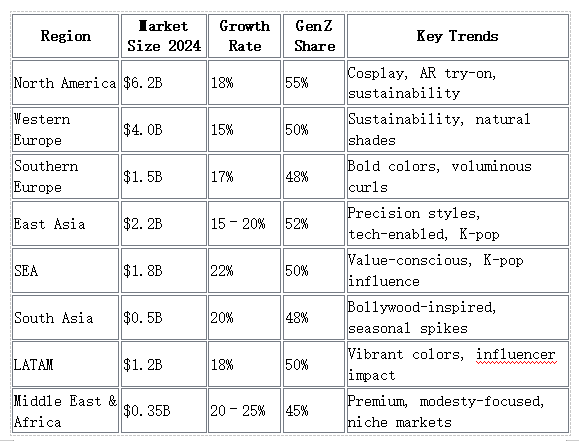

l Market size: $6.2 billion by 2024.

l Gen Z contribution: $3.4 billion (55% of the total).

l Rate of annual growth: 18 % (cosplay & influencer-driven wigs : up to 35% YoY).

Consumer Preferences

l Cosplay wigs: Marvel, anime, and video game were the leading collaborations.

l Afro-textured wigs: Customizable size and density in kinks, curls, coils, and waves for Black hair.

l Rainbo and gradient wigs: Pastel, neon, and fun ombré picks are trending on TikTok and Instagram.

Behavioral Insights

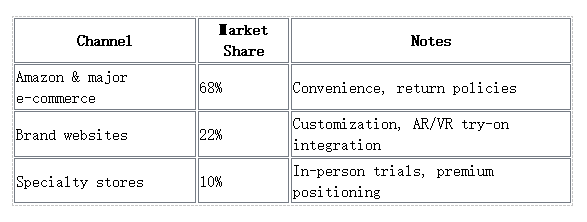

l Distribution channels: Amazon (68%), brand websites (22%), specialty stores (10%).

l Key decision factors: Return policy (72%); Authenticity (65%); Cultural Sensitivity (58%).

l Influencers effect: Micro-influencer campaigns are 3.2x more engaging than celebrity endorsements!

Trends

l AR virtual try-ons adoption is increasing, with 28% higher conversion rates.

l Sustainability Stage: 38% of Gen Z would rather buy wigs made of recycled/biodegradable fibers.

l Male market: Growing male participation, especially in cosplay, gaming, and drag communities.

2.2 European Market: Style Sophistication & Sustainability

Market Segmentation

l Western Europe (UK, France, Germany): Natural shades, subtle highlights, shorter lengths.

l Southern Europe (Italy, Spain): Vibrant colors, voluminous curls, statement styles.

l Northern Europe (Nordics): Minimalist, pastel colors and eco-conscious patterns.

Consumer Behavior

l Price sensitivity: The premium wig market is expanding due to quality and ethical production.

l Distribution channels: Sephora, specialty beauty retailers, and Instagram shopping.

l Online shopping: 43% of Instagram and other social media content influences sales.

Sustainability & Regulatory Influence

l EU Green Deal compliance drives consumer choice.

l Biodegradable fibers and recycled packaging are becoming more and more necessary for acceptance into the market.

Cultural Insights

l Gen Z Europeans were found to be in "high" demand for authenticity and cultural representation.

l Traditional hairstyles were adopted only after the brand provided education on origins.

Innovation Drivers

l Try-on AR filters, virtual stylist apps, curated picks powered by AI.

l Subscription-based and limited edition releases remain staples of exclusivity and on-brand energy.

2.3 East Asia: Japan & Korea – Precision, Technology, and Performance

Market Overview

l Total market: Japan $1.2B, Korea $1.0B in 2024.

l Growth rate: 15–20% YoY.

l Consumption habits: Daily wear, office wear, cosplay and content for social media.

Product Preferences

l Natural-looking wigs: Fringe patch, scalp color-matched base, fine straight hair.

l Functionalities: UV protection, anti-static treatment, moisture retention.

l Customization: Colored, scalp texture simulation, heat-resistant cap.

Consumer Behavior

l High-tech penetration: 65% of purchases are driven by virtual try-apps.

l Accepting the premium segment: $50-$250 per unit for good quality or branded wigs.

Cultural Factors

l Admiration of traditional hairstyles: kimono, hanbok-inspired designs for formal occasions.

l Cosplay culture: Consumption of anime, K-pop, and games.

Distribution Channels

l E-commerce dominates: Rakuten, Kakaku.com, Coupang, Naver.

l High-end specialty stores in Tokyo and Seoul for in-person trial.

2.4 Southeast Asia: Value-Conscious Growth

Market Overview

l Volume: The fastest growing market by volume, particularly for synthetic wigs that are within the range of $20-50.

l Climate issues: Tropical weather demands sweat-proof, breathable caps.

Consumer Behavior

l Get the K-pop effect: Idol replica wigs demonstrate 60% YoY growth in searches.

l Seasonal surges: Weddings, graduations, festivals.

l Social media platforms: TikTok, Instagram, and Facebook for peer reviews and tutorials.

Cultural Integration

l Suitable for hijab compatible wig designs and styles with color for special occasions.

l Focus on modesty and comfort with modern trends in style.

Distribution Channels

l Shopee, Lazada, and Tokopedia are the main players in e-commerce.

l Urban boutiques for the high-end consumer.

Trends

l Micro-influencer campaigns are incredibly successful, with ROI more than three times that of macro influencers.

l K-pop idols are eager to increase their brand visibility with limited-edition collaborations.

2.5 South Asia: Emerging Markets and Aspirational Consumption

Market Overview

l India and Pakistan to be the growth drivers, market size to reach ~$500M in 2024.

l Increasing the disposable income of the Gen Z population for fashion and performance wigs.

Consumer Behavior

l Preference for Cheap synthetic wigs <$15-40 for everyday use.

l Occasional high-end buys ($100-150) for weddings and events.

Cultural Factors

l Bollywood hairstyles influence style.

l Ceremonial demand spikes (weddings, festivals, and religious ceremonies).

Distribution Channels

l Flipkart, Amazon India, and Myntra for online shopping.

l Local boutiques and salons for the high-end segment.

Trends

l AR try-ons are being introduced, but are not very common due to low smartphone penetration.

l Awareness of sustainability is gradually increasing among the urban youth.

2.6 Latin America: Trend Adoption and Community Influence

Market Overview

l Brazil, Mexico, and Argentina leading consumption, ~$1.2B market in 2024.

l Gen Z contributes ~50% of sales.

Consumer Behavior

l High emphasis on color vibrancy and bold styles.

l Influencer endorsements heavily impact purchasing decisions.

Distribution Channels

l Mercado Libre, Amazon LATAM, Instagram shopping for e-commerce.

l Small boutique retailers in urban fashion districts.

Trends

l Cosplay and drag culture increasingly popular, driving diverse styles.

l Biodegradable wigs gaining traction among environmentally conscious youth.

2.7 Middle East & Africa: Niche Segments and Cultural Adaptation

Market Overview

l UAE, Saudi Arabia, Nigeria, South Africa: Developing fashion wig buyers.

l Market size: ~$300–400M in total in 2024.

l Growth rate: 20–25% YoY in urban areas.

Consumer Behavior

l Strong emphasis on premium quality and authenticity.

l Modesty and comfort are considered in the design (use of lightweight caps and breathable material).

l Discovery is driven by social media (ex, TikTok) and peers.

Cultural Factors

l Middle East: Hijab-friendly wigs for the style-conscious.

l Africa: Afro-textured, natural curl wigs for cultural identity.

Distribution Channels

l E-commerce growth: Amazon MENA, Jumia.

l Premium sales are concentrated in specialty salons and beauty retailers.

Trends

l Growth in luxury and sustainable segments, in particular among urban youth.

l Growth among cosplayers and fashion events driven by influencers.

2.8 Comparative Regional Insights

Key Observations:

1. Technology usage has been developed in East Asia and North America the most, and in South Asia the least, as a result of infrastructure gaps.

2. Awareness of sustainability is strongest in Western Europe and is increasing rapidly in North America and East Asia.

3. African and Middle Eastern markets require a great deal of cultural sensitivity, given a variety of hair types as well as religious/cultural norms.

Chapter 3: Product Innovation & Marketing Breakthroughs

3.1 Product Evolution: From Single Styles to Scenario Solutions

Functional Improvements

The Gen Z consumer wants wigs that work for all kinds of situations, climates, and lifestyles. Functionalities have evolved well beyond classic beautification:

Climate Adaptation:

Southeast Asia: Sweatproof and breathable patterns.

Coastal Europe: Wind-resistant design for outdoor events.

Improvements in durability:

Units can be machine washable.

Colorfast treatments that keep their vibrancy after multiple washes.

Comfort Features:

Lightweight caps with stretchable bases.

Designed for comfort during long-term wear, with adjustable straps and memory-fit structures.

Advances in Materials

l Biodegradable PLA Fibers: Aligned with the EU circular economy targets, recyclable or compostable.

l Protein-Based Synthetics: The natural feel, movement and shine of human hair.

l Smart Textiles: Integrating temperature regulation, moisture-wicking fibers and UV protection.

l Hybrid Blends: Human Hair with Synthetic Fibers for strength and style retention at a fraction of the cost.

Customization & Personalization

Customization & Personalization

l AR/AI-driven design platforms enable users to:

Preview color, length and curl patterns in real-time.

Create hairstyles for social media, cosplay, or work.

l A subscription-based service to rotate wigs monthly, tailored to the social calendar and content timeline.

3.2 Marketing Transformation: Community-Centric Approaches

Social Media Ecosystem

1. TikTok Dominance:

#WigTransformation, #HairSwitch and #CosplayReady challenges amassed over 12 billion views worldwide.

Viral content drives word-of-mouth marketing among peers more effectively than traditional advertising.

2. Instagram Authenticity:

Micro-influencer campaigns result in 3.2x higher engagement than celebrity endorsements.

Prioritize BTS content, styling tips and UGC (user-generated content).

3. YouTube Education:

Comprehensive guides on wig installation, care and styling raise confidence to buy by 47%.

Storytelling is woven with tutorials in brands to foster community trust and long-term loyalty.

4. Private Digital Communities:

Discord, WhatsApp and private Instagram communities for sneak peeks, limited edition drops and style advice.

This fosters engagement and builds the brand-consumer relationship beyond a transactional experience.

3.3 Channel Optimization: Omnichannel Experience Design

Digital-First Infrastructure

l Mobile-enabled shopping experiences with one-tap reordering and style recommendations powered by AI.

l Visual search for the instant discovery of styles: whose consumer upload pictures to get the look.

l Inventory Synchronization: You must have accurate quantity of stock using your online store and marketplaces.

Physical Retail Integration

l Flagship stores and pop-up experiences in style-savvy neighborhoods (Seoul, Tokyo, New York, Berlin).

l In-store AR mirrors for instant try-on.

l Workshops and community events to build brand loyalty.

Global Supply Chain Alignment

l Hyper-localized manufacturing hubs that reduce lead time and shipping cost.

l On-demand supply chain production lessens inventory risk and aligns with green goals.

3.4 Technological Integration & Smart Wigs

AR/VR Try-On

l AR try-ons enable 60% of e-commerce wig shoppers to see how wigs look on their faces before they buy.

l The integration of TikTok/Instagram AR filters for social sharing and engagement.

AI Styling Recommendations

l Based on face recognition and skin tone analysis, it recommends colors and styles that match.

l Seasonal updates and trend-based suggestions, e.g., when pastel hues are "trending" on TikTok or a certain cosplay character.

Smart Fibers and Wearables

l Temperature-regulating, UV protective, moisture-wicking wigs.

l With special sensors embedded underneath the scalp, health is monitored and users are alerted to potential problems.

3.5 Sustainability in Product and Marketing

Material Sustainability

l PLA and protein-based artificial fibers for biodegradable applications.

l Minimalistic design and recycled packaging help reduce environmental impact.

Consumer Education

l Advertising campaigns emphasize the associated carbon footprint reduction, circular-economy advantages, and ethical sourcing.

l Brands are capitalizing on sustainability storytelling to deepen emotional ties with eco-conscious Gen Z.

Regulatory Alignment

l The QA is legally correct and market acceptable, considering the compliance with EU REACH and ISO environmental regulations.

l Such certifications (GRS, FSC, OEKO-TEX) give you an extra layer of trust with environmentally conscious consumers.

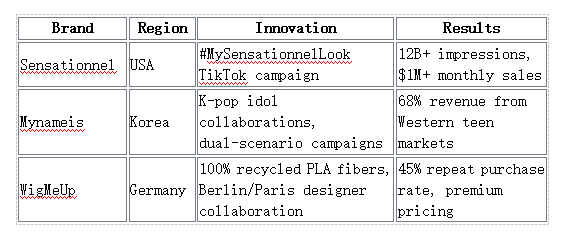

3.6 Case Examples: Marketing Innovation in Action

Key Learnings

1. Content tailored to the local level has a greater impact than global initiatives.

2. Personalization driven by tech leads to higher confidence in purchasing and higher conversion rates.

3. Sustainability efforts improve brand sentiment and willingness to pay a premium.

3.7 Emerging Marketing Trends

l NFT and digital wig ownership: Virtual wigs for avatars on metaverse platforms.

l Collaborations across industries: Gaming, anime, and fashion brands come together for limited editions.

l Content generated by AI: Personalized video ads and style recommendations.

l Commerce driven by community: Peer validation within Discord/WhatsApp groups lead to pre-order and exclusive product drops.

3.8 Summary

Chapter 3 illustrates that the new st